In our series on European Perspectives, partners and members of the EBA will share insights and experiences regarding the blockchain landscape and ecosystem in their area. First up, our partner Amazing Blocks will take us to Liechtenstein where due to the Liechtenstein Token Act every right and asset can become a token. But what about the legal implications? To answer this question, this article introduces and explains the operating principle of the Protected Cell Company (PCC).

One Umbrella Legal Entity for Multiple Assets and Multiple Tokens

With the Liechtenstein Token Act everything, i.e. every right and asset can be tokenized. The question remains, however, how it is legally possible to tokenize everything. To answer this question, this article introduces and explains an advanced tokenization method: Legally compliant multi-asset equity tokenization enabled by a specific holding structure – called Protected Cell Company (PCC). Imagine multiple assets will be tokenized (i.e., multiple real estate objects, multiple machines, multiple IP rights) by one and the same legal entity. Plus, for each asset multiple tranches of tokens are issued (i.e., equity tokens, debt tokens, tokenized participation rights). This way, one real estate object could be represented by both equity tokens and debt tokens. As well as a tokenized machine could be represented by two tranches of debt tokens. The structure of a PCC allows a high degree of flexibility regarding what is to be tokenized. In addition, the Liechtenstein Token Act enables EU passporting, allowing customers simplified market access, which in turn significantly increases operational and regulatory efficiency. Thus shares tokenized in Liechtenstein are regarded both in Liechtenstein and in other countries as normal securities. These are excellent conditions for tokenizing, among other things, equity and representing it with equity tokens. These unprecedented developments, coupled with the new legal certainty provided by the Liechtenstein Token Act, pave the way for the emergence of a token economy.

Tokenizing everything in Liechtenstein

In the blockchain and tokenization space, there are many voices claiming that everything should be tokenized. But this claim falls short. The process of tokenization is nothing less than the transfer of the “old” physical world, with all its goods and assets, into a “new”, digital world. In this process it is of utmost importance that existing law is complied with in order to ensure security and clarity for all parties involved. Hence, the question of how exactly tokenization can be practically implemented, now and in the future, must be addressed first.

The basic structure of tokenization is that an asset or right is represented by a token and the token acts as carrier of this value or right. If shares or equity are tokenized, they are represented by equity tokens. Equally, when debt securities, debt capital or bonds are tokenized, they are represented by debt tokens.

The new Liechtenstein Token Act (TVTG) provides the underlying legal structure and consequently the necessary legal security. This disruptive legislation, which came into force in January 2020, aims to set standards throughout Europe. Liechtenstein is rightly described as a pioneer and forerunner of an emerging token economy. As a result of this well defined jurisdiction, it is now easier to establish trends that are emerging in the field of tokenization. One of these trends is certainly the tokenization of real estate.

Most of the already existing tokenization projects work with debt tokens. The asset – say, a real estate object – is owned by a legal entity and this legal entity is issuing debt. The resulting debt tokens provide an interest payment to the investor based on a fixed interest rate. A flexible interest rate is also possible to accommodate a more beneficial performance. In most legislations, tokenizing debt is basically possible even though complex legal constructs are needed. However, tokenizing equity is more difficult and in most legislations it is still not possible. This circumstance has now changed thanks to the advanced jurisdiction in Liechtenstein. It is now possible to tokenize rights and values of all kinds witout complex workarounds or far-fetched interpretations of paragraphs.

Generally, tokenization is the process of deploying assets and rights on blockchain networks. Tokenization is attractive for investors as it makes investments much more convenient and at the same time allows for much better diversification than before. With tokenization any kind of real assets (e.g., real estate, art, patents, certificates, coupons, cars) can be made investable. Ownership can be fractionalized and fungibility of assets is increased. As a result, efficiency is increased, while at the same time the confidence of the individual actors in the process is strengthened and the costs of those processes are reduced. The issuer on the other hand can “package” all kinds of assets in tokens and offer them to investors. Even individual machines can be tokenized. This would allow investors to invest in single machines. For the machine manufacturer this would be sales financing enabled by the capital market. Each machine can become a single “profit center”. Machines can be financed by investors; made available to customers and – via revenues incurred from the customer – bring return to the investors. As such, the machine as a “profit center” would – like a small company – issue debt tokens and equity tokens. An investor in debt tokens would receive an interest payment for his initial investment while an investor in equity tokens would benefit from the remaining return.

The TVTG provides the necessary legal framework for tokenization processes for the further development of the token economy. Costs and time expenditure are significantly reduced. This is considered a strong driver for the expected mainstream adoption of tokenization in general.

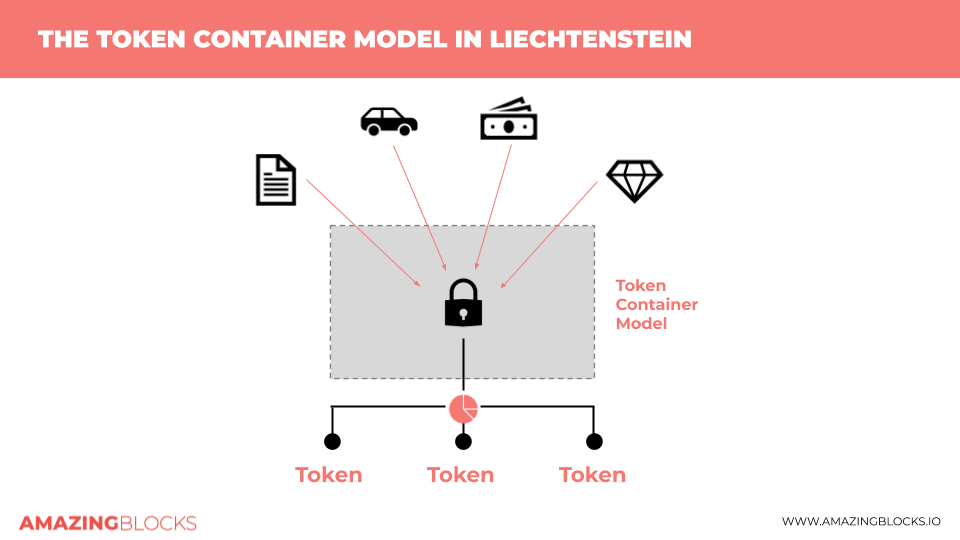

One of the core elements of the new framework is the so called Token Container Model (see Figure 1). In this model a token serves as a container with the ability to contain rights of all kinds. So it is possible to “load” this container with a right that represents a real asset like shares, gold and real estate.

With Liechtenstein being a member of the EEA (European Economic Area), it seems likely that the TVTG will make a decisive contribution to the standardization of tokenization processes in Europe. The regulation recently presented by the European Commission for the regulation of crypto-assets (“Markets in Crypto-Assets” or MiCA in short) deals with a standardized regulation for handling digital currencies and crypto-assets.

An equally important aspect is the issue of custody. If the necessary conditions are met, the holders of the tokens (i.e. the shareholders) are free to choose their preferred custody provider.

Figure 1: The Token Container Model explained

The unique legal framework provided by the TVTG clearly regulates ownership. The owners have the power of disposal over the assets and rights represented by tokens at all times. The tokenization itself follows an ordered life cycle, as do the resulting tokens. This gives software providers like Amazing Blocks the opportunity to offer a wide range of services and products. The cycle in general consists of the following elements: Generating the token, issuing (normally through ETO, STO, IEO or ICO), managing and trading against other tokens, and placing the tokens in an investment portfolio for diversifying purposes from the investor’s perspective.

Protected Cell Company and tokenization in Liechtenstein

Protected Cell Companies enable targeted risk management, as the assets of the individual segments are clearly separated from each other and from the core. PCCs or Segmented Corporate Body (SV) is not a legal form directly, but rather an organizational form that allows corporate bodies to be divided into different segments. The field of activity of the individual segments must be legally permissible and fit the purpose of the legal entity. Due to their perfect fit for structuring financial assets, they are primarily found in investment management. The key of this structure is that each asset can be operated separately in terms of liability and capital although they are all managed by one “umbrella” legal company.

Now when it comes to tokenizing equity, the Liechtenstein Token Act has to be leveraged. Of course, a Liechtenstein-based legal entity is needed for this. For this, a company limited by shares (Aktiengesellschaft) can be used – organized as a PCC. The respective AG’s shares can also be tokenized subsequently. Relying on a tokenization software, the first projects are already doing this which you can read here. These tokenized shares allow an easier administration of the legal entity itself, for example, when it comes to ownership changes or onboarding new investors.

Tokenizing an asset with debt and equity tokens

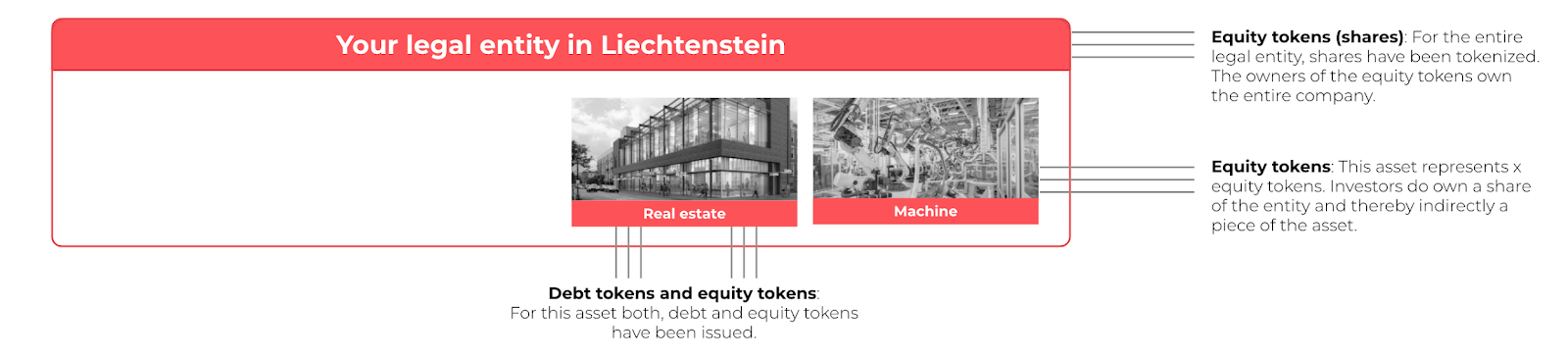

Imagine you place an asset in a legal entity, for example, a real estate object. As described above, this asset can be tokenized by debt tokens which are separated from the tokenized shares of the legal entity itself. Technically speaking, there are two smart contracts at work. One smart contract for the tokenized shares of the company and another one for the debt tokens of the real estate object. A tokenization software provider then allows multi-asset administration.

Another example already mentioned at the beginning is the tokenization of a machine. In this case, equity tokens are a good choice. Here, too, the ownership is transferred to the legal entity and then tokenized. The owner of the token is now the owner of a part of the machine (see figure 2).

Figure 2: Debt and equity tokens of one legal entity

Tokenizing multiple assets with multiple tokens per asset

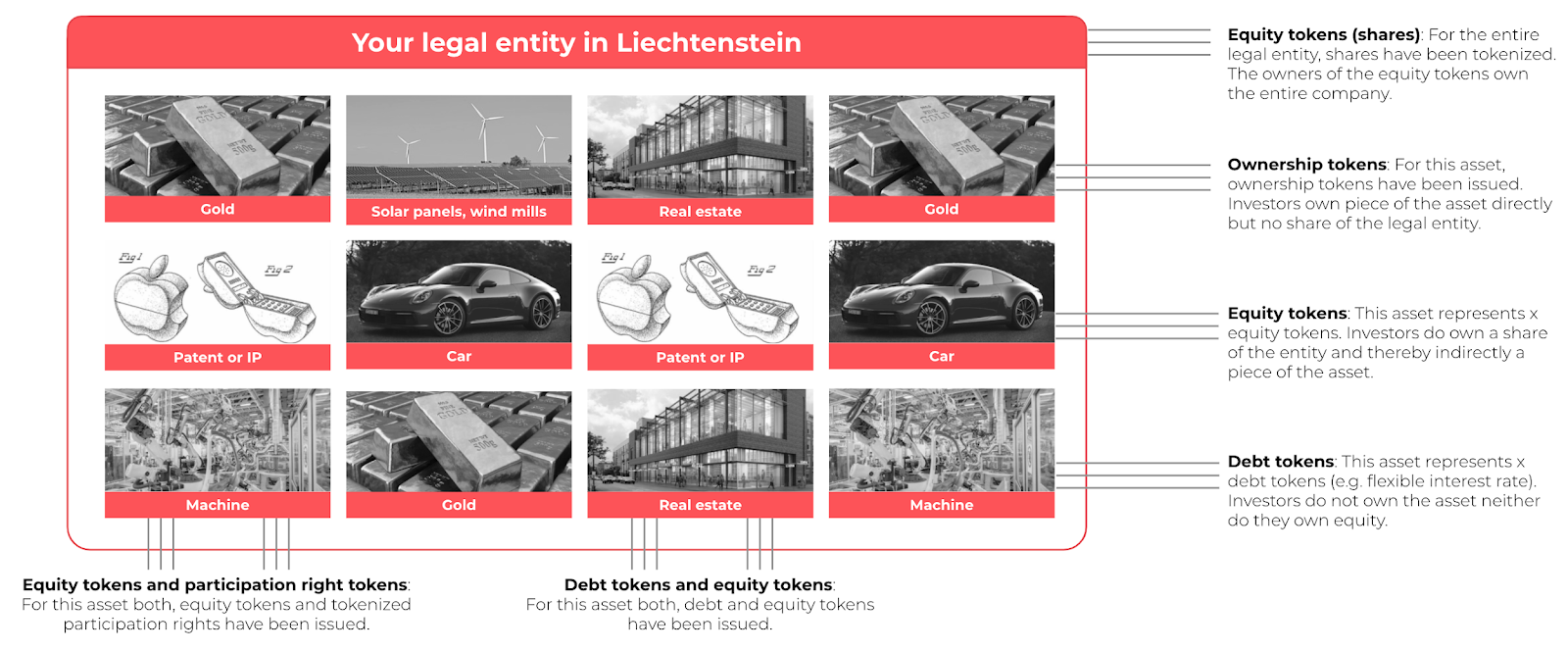

Of course, it would also be possible that we transfer the ownership of multiple assets to the legal entity. Even more so, each asset could be represented by multiple types of tokens. For the machine, equity tokens could be issued. For the real estate object, debt tokens could be issued.

Another very interesting model is if several tranches of tokens are issued for one and the same good. For example, it might make sense for the real estate object to issue both debt tokens and equity tokens. The investors of the debt tokens receive an interest payment for their investment; either a fixed interest rate or a flexible interest rate. Vice versa, the investors in the equity tokens own the asset and hold the equity value. Their reward is – simply speaking – the profit whereas the interest payments have previously been deducted. This innovative multi-asset multi-token emission is illustrated in the following figure 3.

Figure 3: Multi-asset-tokenization

The full picture: multi-asset-multi-token issuance processes

Figure 4 shows the transfer of further assets to the legal entity, which are provided with several tranches of tokens. This process is called the multi-asset-multi-token issuance process. This configuration is a project to be realized in the future. However, it can be assumed that it is only a matter of time before an issuer adopts and applies this lean and flexible solution for asset tokenization.

Figure 4: Multi-asset-multi-token issuance processes

The architecture behind the multi-asset-multi-token issuance process

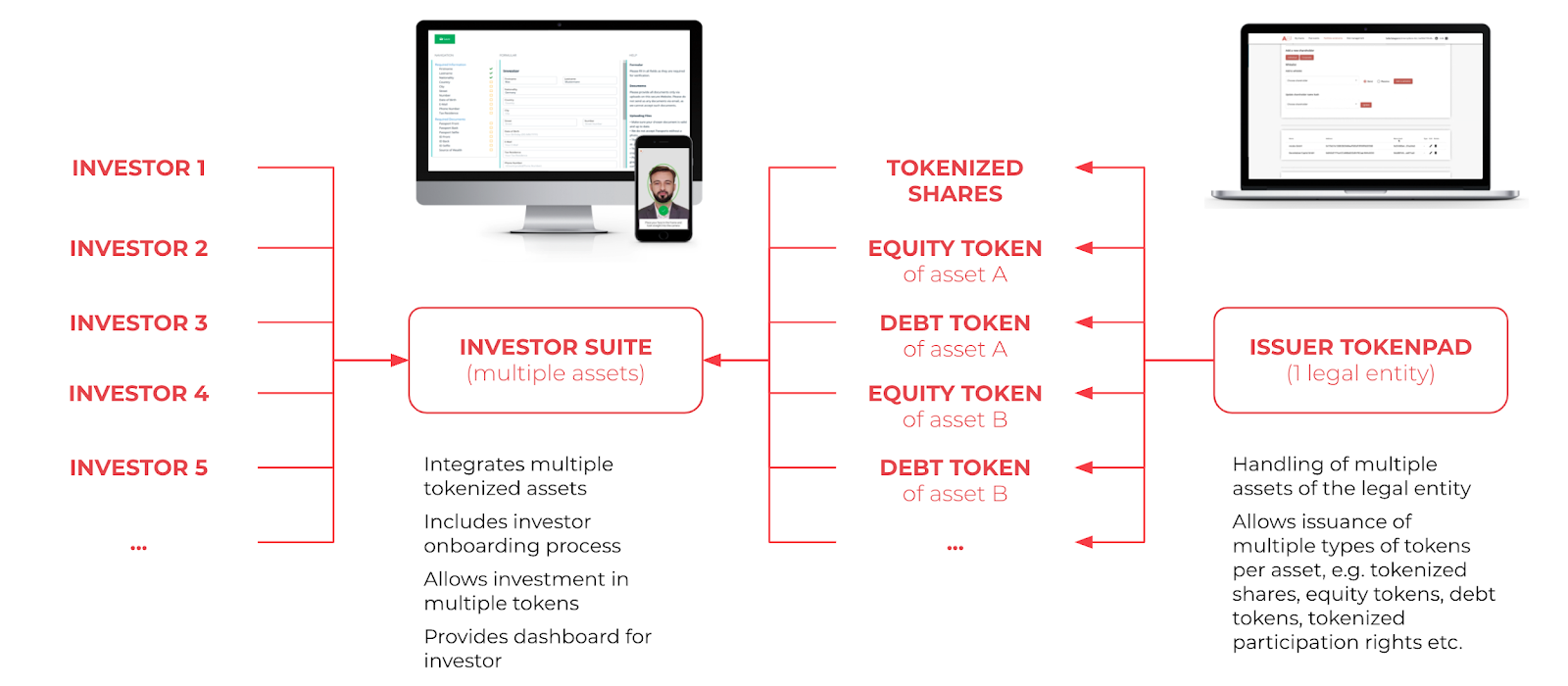

In order to actually be able to cope with this complex model, an advanced tokenization software is needed. On the one hand, this would require an investor suite which will allow investors to onboard themselves and to comply with all required KYC procedures. Once verified, an investor suite integrates multiple assets, allows investments in multiple tokens and of course also provides a dashboard for investors that seek to build a portfolio.

On the other hand, there is an issuer software for the management board. This software allows administering all functions of a smart contract. Tokens generated for an asset stem from a smart contract. If a real estate object or any other asset would be represented by equity tokens and debt tokens, two smart contracts would be in place. Their configurations, the number of tokens outstanding, and token transferral restrictions etc. can be configured with the issuer software. Therefore, it can be used to configure multiple smart contracts to issue multiple tranches of tokens. These tokens such as equity tokens, debt tokens or tokenized participation rights – are plugged in the investor suite, so that investors can invest in them. This is illustrated as follows:

Figure 5: Issuer and investor software establishing a token economy

Conclusion

Liechtenstein has acknowledged that the physical world will sooner rather than later be complemented by a digital world. In a few years, thousands of rights and assets will be represented by tokens. The Liechtenstein Token Act took this inevitable development into account and created the conditions for further development anchored in a proper legal framework. Liechtenstein has secured for itself an exceptional position in the emergence of a token economy.

New asset classes will continue to be discovered and introduced to tokenization. In the process, further new questions regarding jurisdiction will certainly arise. However, the Liechtenstein Token Act has already passed its first practical test and has proven that the framework operates successfully when applied. For the first time, the equity shares of an AG have been successfully tokenized.

A central question that remains is to how equity tokens, debt tokens or tokenized participation rights are recognized and treated in other countries. As a member of the European Economic Association (EEA), compliance with the codified EU/EEA regulations is mandatory. These basic regulations create the foundation on which the Token Act is built.

At this stage it appears that qualified lawyers should be able to find a solution to allow investors from several countries to invest in those tokens generated by or within a Liechtenstein legal entity.

In conclusion, Liechtenstein is already an interesting destination for all kinds of projects focusing on tokenization. The tokenization of rights and assets is now possible in a simple, time-saving, cost-effective way.

Author: Nicolas Weber is Head of Business Development at Amazing Blocks – a tokenization startup from Liechtenstein supporting the entire life cycle: Consulting through the establishment period and a software for issuance, administration and investors. He is your direct contact for any regards. You can contact him via email or connect with him on LinkedIn.

Amazing Blocks offers a tokenization solution that enables its clients to tokenize various assets according to the Liechtenstein Token Act (software-as-a-service). The software covers both the issuance of tokens and investing in tokens. It suits the needs for tokenizing all kinds of assets (e.g. machines, cash flow generating contracts, trademarks, real estate, cars). Imagine that some asset should be tokenized. For this asset various tokens would make sense: Equity tokens, debt tokens, participation rights as tokens, ownership tokens, or any mixture of these tokens. The software of Amazing Blocks helps issuers to handle multiple assets and to issue multiple tokens for these assets. This is possible by integrating blockchain technology with the law (that is, the Liechtenstein Token Act). At the core, there is the “digital legal entity in Liechtenstein” based on “tokenized shares” which allows a very efficient foundation, a very efficient operation of the company and, thus, an efficient and flexible possibility to tokenize assets. This should now make a wide variety of tokenization projects possible, because the costs for tokenization are significantly reduced.